As the art market continues to soar, the art loan has become an emerging source of interest for wealth managers, estate lawyers, banking institutions, art advisory firms, and high-net-worth art collectors. A 2017 survey by UBS, an investment banking company, revealed that 35% of high-net-worth clients were active in the art and collectibles market. However, there is no centrally located place to find information on art loan institutions, including their thresholds and requirements, so Art of Estates collected the most relevant art lending data from some of the top art loan lenders, and here is what the personal property appraisal and consulting firm found during the research process.

Art Lending has Exploded in Recent Years

The art-secured lending market in the United States reached an estimated $17b to $20b in 2017, which represents a 13.3% growth from 2016, according to Deloitte’s Art & Finance report published in 2017. Depending on the situation of the borrower, there are differences between when a private art collector or art gallery wants to attain an art loan from a bank or a business specializing in handling art-based loans. Bank loans often take into consideration many factors of the client, such as their income, credit, and overall financial portfolio. More specialized art loan institutions solely take the features of the unique work of art that the loan is being sought against into consideration when making the contract for the loan. The process of looking over the artwork in question requires a fair market value appraisal, which is what a certified appraiser does for an art loan entity when they are considering the artwork as collateral. Therefore, in the event the client comes under financial stress and is unable to pay off their loan, the only thing liable is the art, not the borrower’s other financial assets. Typically, the art lender would be forced to liquidate the art.

“US has taken the lead in the international development of art-secured lending, taking advantage of the favorable legal environment provided by the Uniform Commercial Code (UCC), tax provisions, and also a different attitude towards the financial aspect of collecting art.”

– Deloitte Luxembourg & ArtTactic Art & Finance Report 2017

Individual Art Collectors are Frequently the Clientele for Art Loans

At many large banks, the clients for art loans are private individuals, as opposed to businesses. These are usually ultra-high-net-worth individuals that typically have an established long-term working relationship with their chosen bank or financial institution. This process is in contrast to other more specialized loan companies in which art dealers make up a large portion of the clientele.

Many art loan companies are popping up in large art cities around the world. In recent years some of these companies have been consolidating. The Fine Art Group in 2019 acquired Falcon Fine Art, becoming a multi-continent art and personal property (only) loan company. This consolidation included the acquisition of ten loans from borrowers ranging from Europe, the United States, and Australia. Since combining the two companies, there has been a steady influx of art collectors calling in to use their art collections as collateral with the company, according to The Fine Art Group.

Many art loan companies are popping up in large art cities around the world. In recent years some of these companies have been consolidating. The Fine Art Group in 2019 acquired Falcon Fine Art, becoming a multi-continent art and personal property (only) loan company. This consolidation included the acquisition of ten loans from borrowers ranging from Europe, the United States, and Australia. Since combining the two companies, there has been a steady influx of art collectors calling in to use their art collections as collateral with the company, according to The Fine Art Group.

Also, in 2019, Carlyle-backed Athena Art Finance was purchased after only four years of operation for $170m by billionaire-backed George Soros’ YieldStreet, which is a digital wealth management company. The art loan space overall clearly continues to be quite active.

Many times, art lending companies allow the client to keep the art or other personal property assets in their home. If the client is living in the United States and the lending company is a U.S.-based company, they will often allow the art to stay in the borrower’s possession or vice versa in Europe. Some companies require the client to store their artwork in a private, secure storage location. The company will provide insurance on the personal property in the event there is a loss, which is in addition to the client’s overall costs for the loan itself.

The insurance coverage carried, at times, results in difficulties as can be seen in the recent situation between Asher Edelman and a French collector. An insurance claim case involving Chicago-based HUB International and Lloyd’s of London. In the event of a loss similar to this situation, it might be wise to read the fine details as to whether or not the receiver of the art loan will be paid out with a full insurance replacement cost or an actual cash value (or fair market value) equivalent in the event of an insurance claim.

Art Dealers Make Up Another Portion of the Clientele for Art Loans

Art dealers make up a portion of the clientele for the art loan industry. Often, they are attempting to use an existing piece of art in their collection as collateral in the acquisition of new promising artwork available on the art market or to cover the costs of running their current art gallery, or to rent space at a costly, but potentially profitable art fair like Art Basel. Frequently art dealers are forced to balance the issue of being obligated to keep their art in one place upon receiving the loan and the need to bring fresher or more trending artworks to these art fairs around the world for selling purposes.

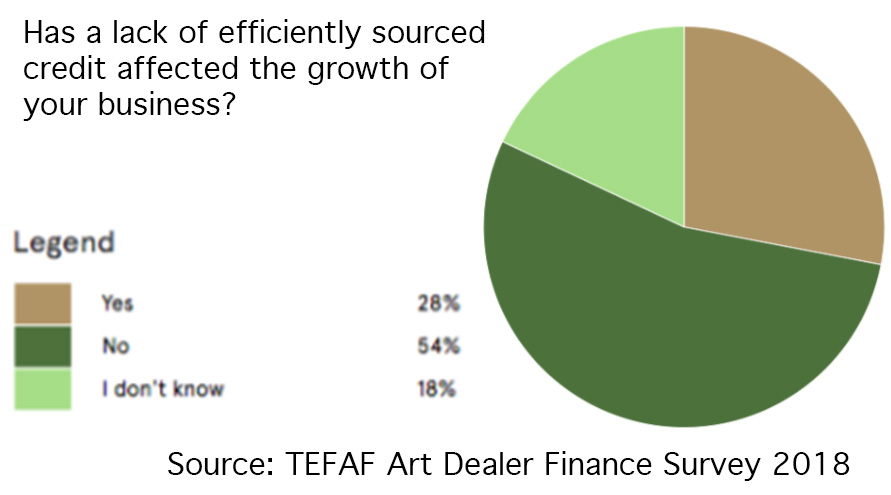

Even though some art dealers are using art lending to pay for expenses, many view it as a high-risk action. Only 4% of dealers said that they regularly use art loans as a way of financing their business. A significant issue with the loaning process to art dealers is the fact that dealers are frequently mistrustful of a lending institution’s valuation of their inventory. The assessment of the artwork is a critical component of the art lending process. Dealers are commonly focused on retail prices as the basis for the value of their artwork, while lenders typically use the more auction market value, which is often considered a faster and more transparent path to liquidity for the art lender. These insightful facts are laid out in TEFAF’s Art Dealer Finance 2018 report, but also something Art of Estates encounters regularly when speaking with art dealers or galleries who are frustrated with the ubiquitous nature of sales through auction houses.

The Size of Art Loans has Increased in Recent Years

Fifteen years ago, art loans were typically offered in the tens of millions of dollars. That number has dramatically changed in time since, with many art loans today numbering in the hundreds of millions. Art loans in the past used to be on a smaller scale, usually around $500,000. Citi Bank reported that art loans typically average around $35 million or more with most clients looking to make investments that are outside of the art market, although some are looking to increase their art collections.

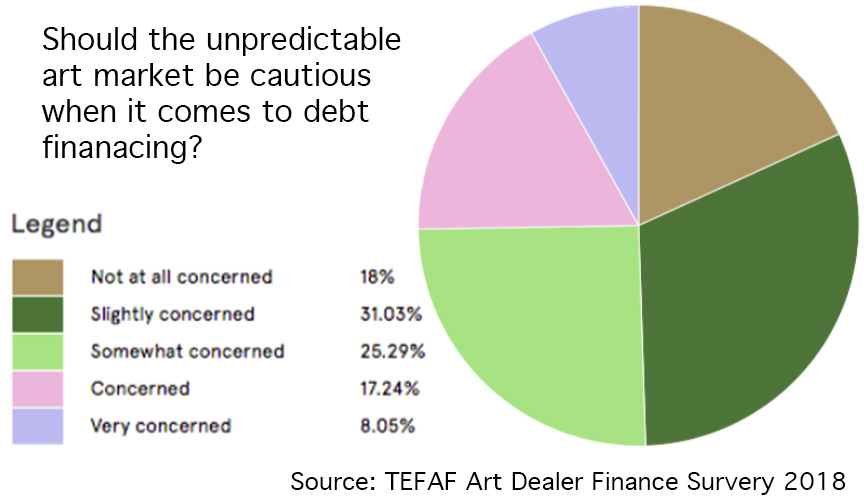

The United States market in the art lending industry is believed to be secure, and it is proliferating in other regions as well, such as Asia and South America. Even with this, the fact remains that outside the United States, the market for art lending is smaller and less established. The situation is due to many things ranging from a lack of established regulations to cultural attitudes towards debt and borrowing.

Certified Appraisers are a Necessary Component of Art Lending, and Just Being a Large Auction House does not Guarantee a Credible Appraisal

Many collectors are finding in the current art market that borrowing against their collection can provide a rapid source of liquidity to use in other investments or debt relief situations. Many new art lenders who are independent of large banks are popping up around significant art cities with big collections such as New York City, London, Geneva, Berlin, and Hong Kong. These companies use the work of art’s liability in terms of its fair market value to determine the potential to loan out money against or loan-to-value percentage. These companies are frequently made up of private investments and have an abundant treasury of potential funds to source out to a client looking to loan out their art.

Art is seen as a low-risk investment because the top of the art market is not as volatile as other markets. When we say the top of the market, as you can see in our data within the excel sheet, the art loan companies are typically looking to loan against art valued at $1m in fair market value and up range. Still, some outsiders have their doubts about lending against art. With the next economic correction looming and depending on how severe the market adjusts; art loan companies could be left holding significant losses on their art loans without a healthy market to sell the artwork. This situation could lead to more oversight and regulations, both of which have support, to different degrees.

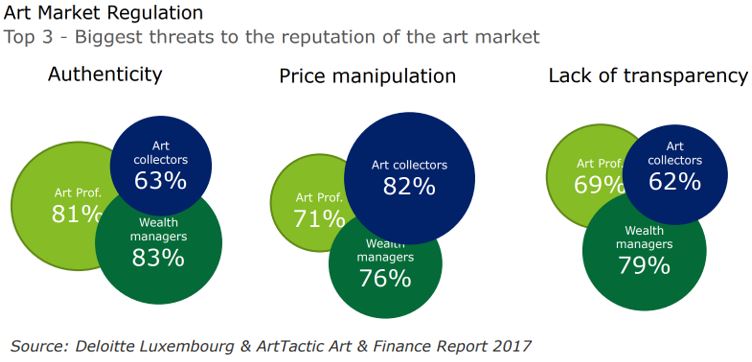

We understand why authenticity is a concern for art collectors, art professionals, and wealth managers. However, we’re surprised that the high-net-worth collectors don’t see authenticity as an issue. Usually, it is the more high-net-worth individuals who are more susceptible to being offered unauthentic art based on art forgery books written on the life of forgers. As for the price manipulation and lack of transparency categories, it also surprises us to see that those areas are such a concern. Of course, shill bidding and guarantees can get in the way of producing an organic auction, this appears to happen at a shallow rate and is often a discernible feature for full-time appraisers. Perhaps the real issue is that the appraisers that they are relying on are not without potential bias (unlike a third party) or fail to have an accreditation or certification in the appraisal industry.

Many of the art loan companies we reviewed did not have accredited appraisers on staff, nor did the affiliated appraisal or art advisory firms have credentialed staff. Some had a minor course, but most failed to have anything but art gallery work, art advisory, or art history degrees. This begs the question of why a reputable institution would loan millions of dollars, but use non-credentialed and untested appraisers so frequently. If these art loan gatekeepers have a vested interest to see the loan through, this automatically places them in a precarious and potentially biased space. We’ve seen what can happen when loan originators and appraisers become too cozy evidenced in the real estate market by the 2008 Great Recession in America.

On July 26, 2019, The Appraisal Foundation, the nation’s foremost authority on valuation services, announced the 9th Circuit Court ruling that agreed with a U.S. Tax Court opinion that found an appraisal from an esteemed auction house is not an adequate assurance of appraisal expertise or competency. Art loan companies should take notice of this ruling arising from the case of Estate of Kollsman vs. Commissioner in which the Estate of Kollsman hired a premier auction house to perform an IRS estate tax appraisal. Evidence showed that the auction house had a conflict of interest (which is against appraisal association standards and USPAP) and that after a competing appraiser was hired, the auction house appraiser manipulated the results of two paintings for which they sought consignment. In other words, they manipulated the price for profit. An unaccredited, non-certified appraiser does not have to abide by rules for which they never agreed, which puts their selected staff of untrained staff in line with the previously mentioned auction house.

While the most significant part of the art loan process, should be researched by a certified appraiser without bias, the art world and art loan companies should continue to gain access to and document clear provenance, a chain of custody, and title rights to the art they use in the lending process. Maecenas claims to be the first open blockchain platform for e-fine art investment (via blockchain-based auctions of fine art). While other entities, like Artory and ArtRights, set up owner cards and establish blockchains for individual pieces of art, the art market at large remains stagnant in defining any one party as an authoritative component to definitive documents related to buying, selling, holding, or loaning against art. RAM (Responsible Art Market) formed in Geneva in 2015, surveyed the art and finance industry in 2017 and they overwhelmingly supported self-regulation, yet not much change has come to the art market at large even though there seems to be a strong consensus.

The Sale-Leaseback Offers an Alternative Way to Partially Liquidate Your Art Collection

Some companies are finding new and creative ways of lending to customers based on their art collections. Artemus (now ArtAssure Ltd.), an organization based in New York City, is one of the companies utilizing a program known as a Sale-Leaseback. This system entails a financial situation in which a person who owns an art collection is prompted to sell a portion or even the entire art collection to a company like Artemus. At that point, the company will lease the art back to the client at a yearly rate. The art collector can re-acquire their collection at any point during the lease for an annual price, which is slightly above the initial sales price.

Lending Institutions are Hesitant to Loan to Art Dealers as Art is Sometimes More Complicated to Sell than other Assets

In terms of lending to art dealers, many banks are exceedingly hesitant. Art dealers can attain finances from private banks as well as asset-based lenders centered in New York City and other cities around the world; however, they frequently still have difficulty acquiring funds. The lack of access to funding is due to many lenders not wanting to risk loaning out money with only a piece of art as collateral. The lack of lending puts art dealers in a tight spot as many of them need the same amount of liquidity that mid-sized businesses do. Lenders are also usually unwilling to lend to art dealers who make the performance of their gallery a central component of their credit support. Utilizing the performance of your business as an asset in attaining a loan is at times referred to as “cash flow lending.” This practice is more commonplace with other types of companies in their acquisition of loans.

One reason that commercial banks are hesitant to lend to art dealers is the lack of transparency in many art galleries and related businesses. A dangerous aspect of lending for many banks is the dependence on what their clients divest to them about how the borrower’s organization is performing. The accuracy of the company’s financial reporting and transparency are critical to these banks’ lending to middle-market businesses. Many art dealers are still not transparent in the performance of their business, although some dealers defy this trend. The waters remain murky in terms of the number of art dealers seeking art loans. The situation in which some dealers are transparent about their business while others are not which affects how loans are made out to art dealers is further expanded upon by Stephen D. Brodie in the TEFAF Art Market Report: Art Dealer Finance 2018,

“Most lenders are reluctant to extend credit to art dealers as ordinary business borrowers. Even the lenders who are comfortable taking art as collateral, are usually unwilling to make loans to art dealers where a key component of the credit support is the performance of the gallery…”

The report further goes on to state that the solution for this issue,

“… practices include audited financial statements from reputable and independent accounting firms, chief financial officers who are far more than mere bookkeepers or controllers, as well as internal controls and systems managed by more than just the principal of the gallery. Many of these things have become common even in the low end of the middle market today, but they are notably lacking among all but the top US art galleries, according to commercial bankers who are active in this space.”

TEFAF Art Market Report: Art Dealer Finance 2018

Another issue an art lending institution may have when loaning to an art dealer is the simple fact that art as collateral is a complicated asset to unwind if the dealer defaults. Adding further difficulties is the fact that the art world at large is not a particularly well-regulated market in terms of buying and selling artwork. A lending institution may be able to make a solid bet on what they might sell a work of art for based on the artist’s secondary market values and doing research into what the artist’s prices are at other galleries (not recommended). Even armed with this information, it is still not as easy as selling other personal property like a designer Hermès handbag or set of Tiffany sterling silver flatware.

These Elements Contribute to Making Art Loan Decisions

Due to our research, several things are clear. Art loans are now more common, and art collectors and art loan companies have come to terms with providing art loans. In other words, lenders and collectors alike are now more comfortable than they ever have been at using art to back a loan for their high-net-worth clients.

The growing art loan industry continues to see progress yearly. According to Deloitte via The Art Newspaper, the Ultra-rich (ultra-high net worth individuals) will spend $2.7 trillion on art by 2026 (7 years). As art loans become more critical to the art industry at large, it’s hard to imagine that regulation will continue to sit on the sidelines. If you are considering your options for an art loan or at least floating the idea, Art of Estates can discreetly and privately provide you with a fair market value certified appraisal. We’ve been providing fair market value appraisals for the IRS with non-cash charitable donations and IRS estate taxes (cost basis), as well as equitable distribution in marital dissolution divorces and even for actual cash value on insurance claims for over a decade.

Click here to find our research on Art Loan companies, which, as a limiting condition, is only relevant to the date it is published.